Fear is in the Air

Written by Eric D. Wanger

This essay by Eric D. Wanger was originally published in a newsletter for the financial clients of the multifamily office he ran in Chicago. Inflation finished at 1.5% for 2010.

July 1, 2010

On a recent research and marketing trip through the West, I was impressed by how much fear I saw. Investors of every level of sophistication and experience were terrified, deeply afraid of where the markets might go. The irony is that no one I talked to could agree on what to be afraid of. Some were terrified of an impending stock market crash, some of a double-dip recession, some of the weight of future taxes, some of a socialist revolution, some of the religious right, some of anti-immigration vigilantes, some of pro-immigration scofflaws, some of the wars, some of the terrorists, some of the impending hyperinflation, and some of deflation. Wait, what was that last one? Deflation?

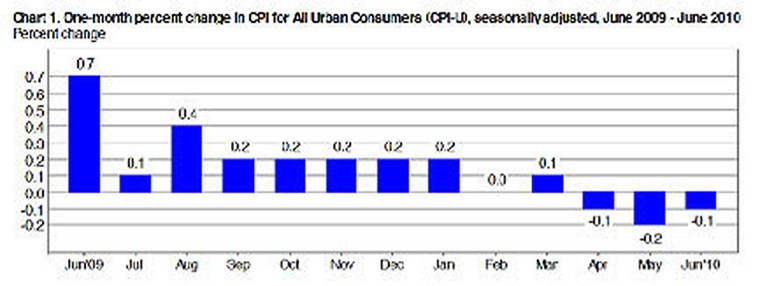

It’s true: Deflationary fears have been making the headlines. But unless you have been following Japanese economics it’s unlikely you have thought much about deflation or even know exactly what it is. During the second quarter of 2010, the consumer price index went negative for three months in a row, and there is no reason to think the trend is over. This scares economists and policy makers, because deflation often goes right along with recessions, and tends to extend periods of unemployment, excess capacity and sluggish development. But what exactly is deflation and why should we be nervous about it?

Seasonally Adjusted One-month Percent change in CPI for All Urban Consumers (June 2009-June 2010)

Source: Bureau of Labor Statistics, CPI News Release, Consumer Price Index, July 16, 2010.

Definition of Deflation

In economics, deflation is a decrease in the general price levels of goods and services. As one might expect, this is the exact opposite of inflation. Deflation occurs when the rate of change in general market price levels goes negative (i.e. the inflation rate falls below zero percent). So saying we’re in a deflationary period is exactly the same thing as saying we’re experiencing a negative inflation rate.

For people used to inflation, deflation seems upside-down. In deflation, the real value of money increases while you sleep, allowing one to purchase more goods and services tomorrow than with the same amount of money today. Over time, deflation actually increases the purchasing power of the money in your pocket. That sounds great. So how could anything that good be bad for us?

Source: Bureau of Labor Statistics, CPI News Release, Consumer Price Index, July 16, 2010.

Negative Effects of Deflation

Unfortunately, our way of life works a lot better when the economy is growing. Deflation is correlated with (although not necessarily caused by) recessions. This includes the Great Depression. One way to think about deflation is as a generalized glut of everything. In a deflationary environment, there seems to be too much of everything available for purchase, rental or hire. Thus, there is no need to buy equipment, hire employees or borrow money. In a deflationary world, the only way to compel a buyer to buy is to lower prices because there is simply too much of everything already in the marketplace. While this is an oversimplification, it is easy to imagine a no-growth world in which people have as much housing as they want to buy, firms have as many employees as they wish to hire, and banks have more available capital than customers want to borrow.

Deflation also means that credit will cost more than it first appears. Real interest rates will exceed nominal interest rates, creating an invisible increase in a loan’s actual interest rate. For example, if deflation averages 10% per year (like certain periods during the Great Depression), a loan would have to be paid back in dollars costing 10% more each year. So even if nominal interest rates are quoted very low, it can be quite expensive to borrow money. In an inflationary world, loans actually cost less than they appear because one can pay them back with dollars worth less than at the beginning. In a deflationary environment, this benefit gets turned upside down. And if credit is expensive, individuals and firms will not find it worthwhile to borrow money to build, expand and invest.

The realization by consumers and firms that a dollar tomorrow might actually be worth more than a dollar today creates a strong incentive to save and not spend. In a consumption-driven economy, that is bad news for people making or selling houses, refrigerators, ski trips and country club memberships. Right now, the U.S. personal savings rate is higher than it has been in a long time, reaching over 6% in the second quarter. The good news is that people are acting more responsibly with their money: People have much less credit card debt, are borrowing less for homes, and are generally saving more money. The bad news is that our economy still needs to reflate from the last few years of economic slowdowns. A bit of wanton spending wouldn’t be so bad for the economy right now. FYI, that’s not liberal claptrap. It was Milton Friedman who famously suggested fighting deflation by dropping money from helicopters!

Scaring the Children

The ultimate deflationary boogey-man is the deflationary spiral. In this situation, price decreases lead to lower production by firms. Lower production leads to lower wages. Lower wages lead to lower economic demand. And lower economic demand leads to further price decreases. This vicious cycle is like the flat spin of an airplane. There is little the pilot can do but watch helplessly as he slowly and elegantly spins down into the ground. Some economists believe that the Great Depression was a deflationary spiral, caused or exacerbated by particular policy mistakes, resulting in a decreased money supply and a generalized glut of everything.

It is common economic wisdom that a better response to looming deflation is to flood the economy with increased money supply and to engage in quantitative easing, a policy wonk’s term for all of the various ways the government can stimulate money supply growth and increase aggregate demand.

An Illustrated Dictionary of Aviation, edited by Bharat Kumar, McGraw-Hill Companies, Inc.

Central banks, starting with our Federal Reserve, use short-term interest rates (like the overnight federal funds rate) as their primary lever to stimulate lending, which increases the money supply in the economy. This would generally be expected to get the economy moving again. But what happens when the interest rate is already zero? What if there is nowhere lower to go? This is not an imaginary scenario. The Fed funds rate is effectively at zero in the U.S. right now.

Gauti Eggertsson, an economist at the New York Fed, wrote that the old Keynesian school taught that the economy could become stuck in a liquidity trap, a scenario in which the government is effectively out of meaningful stimulus options. Eggertsson defines a liquidity trap as “a situation in which the short-term nominal interest rate is zero.” The theory was that once interest rates reached zero, the money supply could no longer be stimulated, creating an economic death spiral. Luckily, modern economists are no longer that bleak. Eggertson, discussing the modern view of the liquidity trap, states:

The modern literature, in contrast, emphasizes that, even if increasing the current money supply has no effect, monetary policy is far from ineffective at zero interest rates…. According to the modern view [of the liquidity trap] outlined above, monetary policy will increase demand at zero interest rates only if it changes expectations about the future money supply, or equivalently, the path of future interest rates.¹

¹Source: Eggertsson, Gauti B. “Liquidity Trap.” The New Palgrave Dictionary of Economics. Second Edition. Eds. Steven N. Durlauf and Lawrence E. Blume. Palgrave Macmillan, 2008.

Ironically, this idea means that expected inflation cures deflation! Even if short-term interest rates are at near-zero, the expectation for future inflation can stimulate aggregate demand by incentivizing individuals and businesses to borrow, spend and invest in growth. They might as well spend money now since their dollars will be worth less in the future.

As then-Federal Reserve Governor (and current Fed Chairman) Ben Bernanke said in 2002, “sufficient injections of money will ultimately always reverse a deflation.”

Over the last two years, we have witnessed the Fed funds rate go nearly to zero, direct support for big bank balance sheets, direct participation in the bond and mortgage-backed security markets by the Treasury, and direct transfer payments to the states. Policy makers claim that all of this quantitative easing kept us out of the abyss. True pessimists believe that, despite all this, the U.S. economy will slouch into a period of stubborn deflation as banks aren’t lending again and businesses and consumers aren’t spending.

Everyone is Afraid of Something

In an inflationary world, people shop at lunchtime because their paychecks won’t go as far by dinner time. However, in a deflationary environment, your money will be worth more at dinner and even more at breakfast tomorrow. The problem with deflation in a modern economy is the cost of borrowing goes up, the value of collateral goes down, and individuals and businesses are incentivized to save rather than spend. This is not a good way to create jobs and generate economic growth.

On one side, we have those concerned about deflation, fearing that widespread price declines, oversupply and general deleveraging will continue to be a powerful disincentive to bank lending, corporate spending and economic growth. This group believes (with plenty of evidence) that the U.S. may become stuck in a no-growth, oversupplied, over-labored quagmire in which the only way to put land, labor or capital to work is by lowering prices.

On the other hand, we have people terrified of inflation and taxation. This group believes (with plenty of evidence) that the U.S. will slingshot out of this recession into a period of horrible inflation, the ultimate bust of the dollar, and a raging thirst for taxing everything in order to pay for the ballooning national debt and entitlement programs.

The irony is that the two groups need each other. If the only way to get out of deflation is the expectation of inflation, then the deflation-fearing policymakers need people to expect inflation. Likewise, the only way to cool inflation is if people expect things to cool off.

That’s the riddle for policy makers, and maybe it’s why so many smart and experienced people can disagree as to what the future holds. Fear is overwhelming us right now, but it is unclear what to fear more: the inflation, monetary debasement, excessive debt and rising interest rates scenario that scared us last year, or the stalled, deflationary, no-growth economy that many fear now. Luckily, I think, we’re afraid of both.

It is often said that the world of finance cycles endlessly between fear and greed. We are definitely doing fear right now. Fear and risk aversion are in style this season. Growth and risk-taking are clearly out of style. Everyone is afraid of something right now—but nobody can seem to agree on what to be afraid of.

Our advice: Keep your head and don’t panic. A temperate middle course is generally the right answer, especially in times like these. Long-term investors will see many excellent opportunities over the next year. But it will take patience to resist bad deals along the way, and even more patience to allow the long-term seeds to blossom.

Eric D. Wanger, JD, CFA